We aim to provide you with value every step of the way.

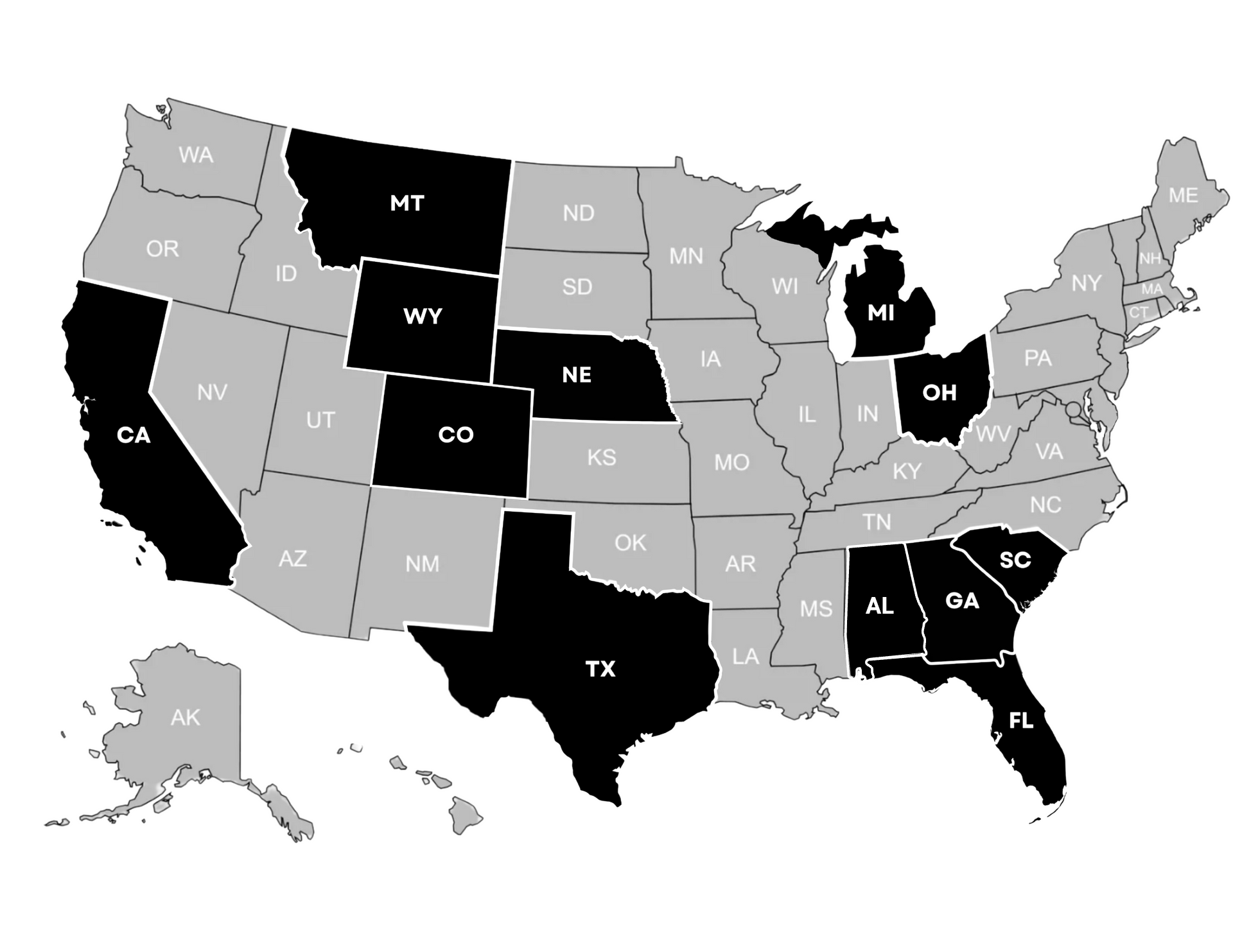

States We're Licensed In

California

Colorado

Florida

Georgia

Michigan

Montana

Nebraska

Ohio

South Carolina

Texas

Wyoming

Your actual rate, payment, and costs could be higher. Get an official Loan Estimate before choosing a loan.

Monthly payment disclaimer:

Your actual savings will vary. Monthly Payments do not include taxes and insurance. Your payment obligation will be higher.

Refinance claim to reduce monthly payment and interest disclaimer:

As a result of refinancing, your total finance charges may be higher over the life of the loan.

Rate of interest disclaimer:

The stated rate may change or not be available at the time of loan commitment. Lock-in is needed.

FAQs

-

How do I qualify for a home loan?

Your lender will compare your monthly income to your monthly debts, including a new home payment, to determine your eligibility for a mortgage. A solid credit history is also necessary. These will decide what you can afford in terms of a home's price and monthly payment, along with your capacity to contribute various down payment amounts.

-

How do I qualify for a conventional loan?

Eligibility for a conventional loan depends on having at least a 620 credit score. However, to qualify for the best rates, borrowers must often have a credit score of 740 or higher.

-

How do I qualify for an FHA loan?

To qualify for an FHA loan, borrowers need regular work that will cover the mortgage payment and other bills. Additionally, a standard prerequisite is a credit score of 580.

-

How do I qualify for a home loan as a first-time buyer?

If you have never owned a home or you have owned a home, but it has been over three years, then you qualify as a first-time home buyer.

-

How do you compare home loan rates?

It is crucial to compare your options on the same day because home loan rates fluctuate daily (and even many times each day) depending on the loan type. Your objective should be to identify the loan type and term that best meet your needs and have a down payment that you can afford.

-

How do you compare refinance mortgage rates?

Describe the item or answer the question so that site visitors who are interested get more information. You can emphasize this text with bullets, italics or bold, and add links. -

How do you compare refinance mortgage rates?

When refinancing, you should focus on the new rate and the monthly savings compared to the fees involved in obtaining the new loan's terms. Be sure to strike a balance between your savings and expenses. Your loan originator can assist you in deciding which choice is better for your financial objectives.

-

How do I compare mortgage rates without hurting my credit score?

A common myth is that your credit score drops every time a credit report is run. While this may be true for revolving loans, such as credit cards, it is rarely the case when pulling credit for a mortgage. Mortgage lenders appear differently on your credit report, and even if several mortgage lenders inquire about your credit, only one credit inquiry is recorded if done within a three-week period.

-

Do you need a perfect credit score to buy a home?

No, you still have choices for purchasing a home with a credit score as low as 580.

-

What loan program requires the lowest credit score?

VA and FHA home loans tend to require the lowest credit score at 580. However, these loans also come with additional prerequisites to qualify for their use.

-

Why doesn't my lender's credit score match the credit score I see for myself?

The credit score lenders use differs from the one you might access online, so you should request a credit check from a lender.

Common Mortgage Terms

-

Amortization

Amortization is the process of paying installments toward a loan over a set time, such as a mortgage. Each installment pays off a portion of the principle while the remainder goes toward interest. A standard home loan may amortize over a 15, 20, or 30-year term. When a loan fully amortizes, it has been paid off in full by the end of the amortization schedule.

-

Annual Percentage Rate

An annual percentage rate (APR) is the cost of borrowing money for a mortgage. The APR is a broader measure than the interest rate alone because it includes the interest rate, discount points, and other fees associated with the loan. An APR provides a more accurate image of the loan's true cost.

-

Adjustable-Rate Mortgage

An adjustable-rate mortgage (ARM) is a loan with an interest rate that changes based on market rates. Borrowers initially receive a fixed interest period when signing up for an ARM. This is the loan's introductory period, which can last up to ten years. During the initial period, your interest rate is typically lower than that of a fixed-rate loan. After the introductory period, the interest rate is determined by market interest rates.

-

Appraisal

Mortgage lenders require an appraisal before signing a home loan agreement, which is a rough estimate of the value of your home. The appraisal ensures that the lender is lending you only what your home is worth. Your lender can assist you by scheduling an appraisal by an independent third party.

-

Assets

An asset is anything you own with a cash value in the context of a mortgage. A lender will want to verify assets when someone is looking to take out a mortgage loan. This ensures that you have enough money saved and invested to cover your mortgage if a financial emergency occurs.

-

Balloon Loan

Balloon loans, or a balloon mortgage, require a lump sum payment at some point during the mortgage term, usually at the end. With a balloon loan, you can pay either an interest-only mortgage or one including both principal and interest payments. Interest-only mortgages require you to pay only the interest cost during the term, with the entire balance due at the end.

-

Closing Costs

Closing costs are the upfront, out-of-pocket expenses associated with obtaining a mortgage. They cover various costs incurred at the time of loan signing or closing. Closing costs often include but are not limited to an origination, appraisal, credit report, and title search fee. Homebuyers typically pay closing costs, but in some cases, sellers may cover some of the costs.

-

Closing Cost Disclosure

A Closing Disclosure is a document that details the final loan terms. This document contains your interest rate, loan principal, and closing costs. Before signing the dotted line, by law, lenders must give borrowers at least three days to review the closing disclosure.

-

Debt-to-Income Ratio

The debt-to-income (DTI) ratio measures a borrower's ability to repay a mortgage which is calculated by totaling all monthly debt payments and dividing the total by the gross monthly income. Many lenders prefer borrowers to have a DTI ratio of no more than 43%, but this figure is somewhat flexible.

-

Deed

A deed is a physical document proving you own your home. When your loan is closed, you will receive your deed.

-

Discount Points

Discount points are a type of closing cost that you can pay to "buy" a lower interest rate. One discount point equals one percent of your loan amount. The more discount points you purchase, the lower your interest rate. Borrowers must pay for them in cash at closing if buying more points.

-

Down Payment

A down payment is an upfront payment of the home's purchase price paid by the buyer. Buyers often put down a percentage of the home's value as a down payment and then borrow the remainder through a mortgage. A larger down payment increases borrowers' chances of obtaining a lower interest rate.

-

Earnest Money

Earnest money is a deposit paid by the homebuyer when entering into a purchase agreement for a house, usually as a sign of good faith. The deposit is generally held in an escrow account by the title company. Earnest money gets applied to the down payment or closing costs when the home is sold. If the sale fails, the earnest money is given either to the buyer or seller, depending on whether the reason for the termination was allowed in the purchase agreement.

-

Escrow

An escrow account, also called an impound account, holds a portion of the borrower's monthly mortgage payment to cover homeowners insurance premiums and property taxes. The mortgage lender will usually set up an escrow account for insurance and taxes and make payments on the borrower's behalf. This system ensures these bills are paid and allows the borrower to make small monthly installments rather than large payments once or twice a year.

-

Fixed-Rate Mortgage

If the homeowner has a fixed-rate mortgage, the interest rate stays will not change over the life of the loan. Homeowners who choose a fixed-rate term frequently believe that interest rates will rise over the duration of their loan and value the stability and predictability that this type of loan provides.

-

Loan Estimate

A loan estimate is a standard document containing mortgage details. It is provided to borrowers when they apply for a loan. The loan estimate includes the interest rate, monthly payment, total closing costs estimates, taxes, insurance, prepayment penalties, and other important loan information. The loan estimate can help compare terms when shopping for a mortgage; receiving one does not imply that they have been approved or denied the loan.

-

Loan-to-Value Ratio

Mortgage lenders use the loan-to-value ratio, or LTV ratio, to compare the loan amount to the property value. An LTV ratio of 80% or less, which corresponds to a 20% down payment, is ideal. FHA or VA loans often allow for higher LTV ratios and may or may not require mortgage insurance.

-

Mortgage Term

A mortgage term is how long the borrower will pay toward the loan before fully owning the home. For example, if a borrower has a 30-year term, they will make monthly payments on the loan for 30 years before it matures.

-

Pre-Approval

A pre-approval is a document that indicates how much someone can afford to borrow for a home loan. Many lenders regard pre-approval as the first step in obtaining a mortgage. When applying for pre-approval, the lender will ask about credit score, income, assets, and other financial information. The lender uses the information to determine the amount the borrower qualifies for in a home loan. This can provide you with a rough budget to use when comparing properties.

-

Principal

The amount borrowed is referred to as the principal balance. For example, if you buy a house with a $450,000 loan from your lender, your principal balance is $450,000 and does not include interest.

-

Private Mortgage Insurance

Private mortgage insurance (PMI) is insurance meant to protect lenders in case of a loan default. If the borrower puts less than 20% down, the lender will usually require the borrower to pay PMI. When 20% equity in the property is reached, PMI can usually be removed from the loan.

-

Property Taxes

Your local government will require you to pay property taxes. Property taxes help pay for police departments, roads, libraries, and community development projects. The amount of property taxes you pay is determined by the value of your home and where you live.

-

Refinance

A refinance occurs on an existing mortgage. Borrowers can use refinancing to make a more convenient payment schedule, lower the interest rate, or choose a different term. In essence, you exchange the original debt obligation for a new one.

-

Seller Concessions

A seller concession is a clause in your offer that request the seller to pay for specific closing costs. For example, you could ask the seller to pay appraisal fees or a title search. The seller may reject your concessions or send you a counteroffer that excludes the concessions. The percentage of your closing costs that sellers can cover varies by property type.

-

Title

A title proves that you own a house. Your title contains a physical description of your property, the names of anyone who owns it, and any liens against it. When someone says they are "on the title" to a house, it means they have legal ownership of the property. For example, if your parents assisted you in purchasing a home, they would almost certainly be listed on the title.

-

Title Insurance

Title insurance is a typical closing expense. You purchase title insurance to protect yourself from third-party claims on your property. Unlike other types of insurance, title insurance does not require monthly payments. Instead, the borrower makes a single payment at closing to protect you for the duration of your home ownership.

-

Loan Estimate

A loan estimate is a standard document containing mortgage details. It is provided to borrowers when they apply for a loan. The loan estimate includes the interest rate, monthly payment, total closing costs estimates, taxes, insurance, prepayment penalties, and other important loan information. The loan estimate can help compare terms when shopping for a mortgage; receiving one does not imply that they have been approved or denied the loan.

-

Loan-to-Value Ratio

Mortgage lenders use the loan-to-value ratio, or LTV ratio, to compare the loan amount to the property value. An LTV ratio of 80% or less, which corresponds to a 20% down payment, is ideal. FHA or VA loans often allow for higher LTV ratios and may or may not require mortgage insurance.

-

Mortgage Term

A mortgage term is how long the borrower will pay toward the loan before fully owning the home. For example, if a borrower has a 30-year term, they will make monthly payments on the loan for 30 years before it matures.

-

Pre-Approval

A pre-approval is a document that indicates how much someone can afford to borrow for a home loan. Many lenders regard pre-approval as the first step in obtaining a mortgage. When applying for pre-approval, the lender will ask about credit score, income, assets, and other financial information. The lender uses the information to determine the amount the borrower qualifies for in a home loan. This can provide you with a rough budget to use when comparing properties.

-

Principal

The amount borrowed is referred to as the principal balance. For example, if you buy a house with a $450,000 loan from your lender, your principal balance is $450,000 and does not include interest.